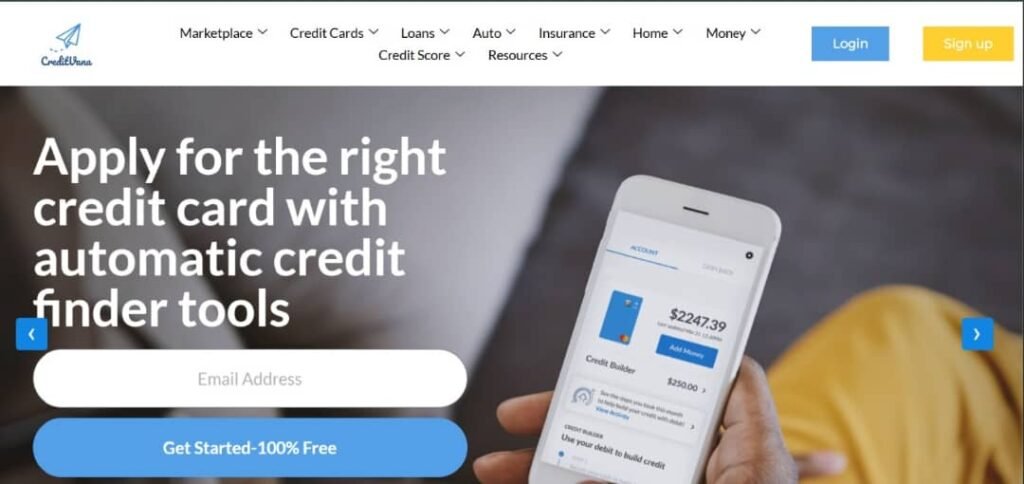

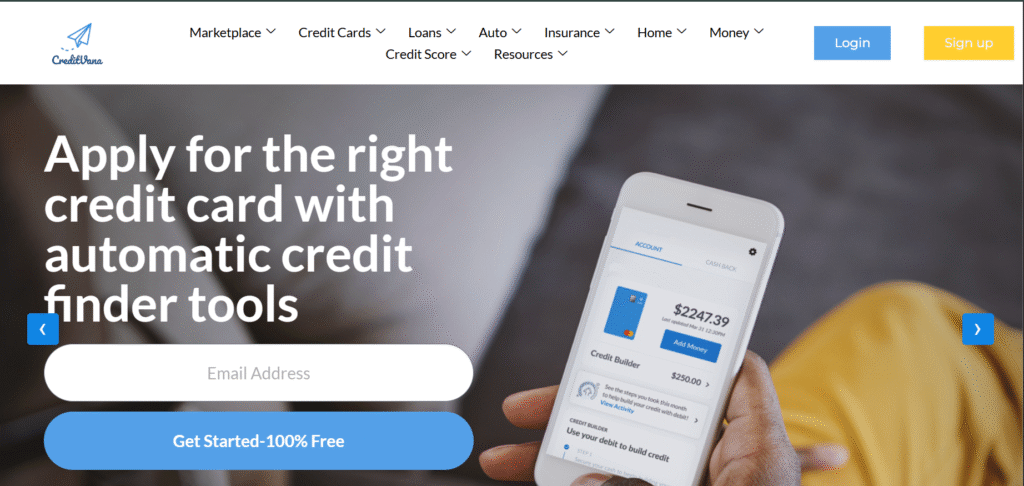

CreditVana is a fintech platform that provides credit monitoring and credit score services, with a strong emphasis on being free. According to its website, users can check their credit scores and reports from all three major credit bureaus — Experian, TransUnion, and Equifax — without paying a subscription fee. CreditVana+2CreditVana+2

It also offers a mobile app (available for both iPhone and Android) that gives real-time credit updates, alerts, and a “credit report card” that helps users understand what factors are influencing their credit scores. Digital Journal+2CreditVana+2

Recently, CreditVana launched version 5.2.0 of its app, which introduces a marketplace for credit-building products: credit-builder accounts, credit cards, and other credit-related offerings. CreditVana This makes it not just a passive credit tracker but a tool for actively building or improving credit.

How CreditVana Works

Here’s a breakdown of how CreditVana functions and what services it provides:

- Credit Monitoring & Scores

- It offers 100% free access to credit scores. CreditVana+1

- It claims to pull scores from all three major bureaus (Experian, TransUnion, Equifax), which, if true, is a more comprehensive approach than many “free” credit services. FinancialContent+1

- Users are given regular updates via AI-powered technology. According to CreditVana, its AI continuously analyses data to alert users when there are meaningful changes. CreditVana

- Credit Report Card

- The “report card” shows what factors are impacting a user’s credit (for instance, credit utilization, payment history), giving insights into how to improve. Creditvana+1

- This transparency helps users understand not just what their score is, but why it is that way.

- Alerts & Security

- CreditVana provides free credit monitoring alerts. Users are notified of suspicious activity or significant changes to their credit, which can help them catch potential identity theft or damaging reporting early. CreditVana

- The site suggests that users can check their scores daily to stay on top of any changes. CreditVana

- Credit-Building Marketplace

- The newer app version (5.2.0) has introduced a marketplace feature where users can browse credit cards, credit-builder accounts, and similar credit products. CreditVana

- Users can apply directly within the CreditVana app for the products listed, making the process smoother. CreditVana

- Once someone is approved, they can track how their payments and the new account are being reported to credit bureaus, which helps them monitor credit-building progress. CreditVana

- Financial Education & Recommendations

- CreditVana’s platform doesn’t just give raw credit scores; it also gives actionable recommendations based on your credit profile. By analyzing your data, the AI suggests steps to build or repair credit. Venture World+1

- Because of the marketplace, users can match with credit products tailored to their credit profile, making the financial advice more personalized. CreditVana+1

- Business Model

- The core offering for users — credit monitoring and score access — is free. CreditVana explicitly advertises “no monthly fees, no hidden costs.” CreditVana

- Presumably, CreditVana makes money through the marketplace: when users apply for credit-builder accounts, credit cards, or loans through their app, CreditVana may receive referral fees or partner commissions from financial institutions. This is a common model among fintech credit-score platforms.

- By incentivizing users to use the marketplace, CreditVana can monetize without charging consumers directly, which aligns with their “free forever” promise.

Strengths & Advantages

CreditVana has several compelling strengths:

- Truly Free Access: Many credit-monitoring services charge monthly or have “free trials.” CreditVana’s pitch — free scores from all three bureaus — is very attractive. Digital Journal+1

- Comprehensive Credit Picture: By offering data from all three major bureaus, it gives a broader and more accurate view of credit health than services that rely on only one bureau. openPR.com+1

- AI-Powered Insights: Their AI seems to provide sophisticated analysis, helping users interpret their scores, understand the drivers of their credit, and receive alerts. CreditVana

- Credit Building Tools: The built-in marketplace makes it easy to find credit products that actually help users build or repair credit. Rather than just telling you your score, they help you do something about it. CreditVana

- User Experience: According to their press materials, the app is designed to be clean, mobile-first, and easy to navigate. The Chronicle-Journal

- Large User Base & Social Proof: Their website claims over 17 million users and 323,000 five-star reviews. Creditvana

- Security Focus: They highlight free monitoring and notifications for changes, which is useful for identity theft protection.

Risks, Concerns & Caveats

While CreditVana presents many positives, there are several things to be cautious or skeptical about:

- Business Model Dependency

- Since CreditVana doesn’t charge its users, it likely depends on partner revenue (from credit cards, lenders, etc.). This could influence which products it recommends, potentially biasing towards those that pay CreditVana more, rather than what’s best for the user.

- Accuracy Claims

- CreditVana claims “real scores” from the three bureaus and uses AI to produce “highly accurate” reports. While plausible, it’s hard to independently verify how precise their “real-time” scoring is compared to traditional tools — especially since many lenders use different scoring models. They claim to mirror “lender-used scoring models” via AI. CreditVana

- If their algorithm is wrong or not fully aligned with what lenders use, users might get a misleading picture of their credit risk.

- Privacy and Data Use

- Any service that aggregates credit data must handle sensitive personal data. While their site mentions terms of use and a privacy policy, it’s important for users to review exactly how their data is stored, used, and potentially shared with partners.

- The affiliate link you shared (creditvana.pxf.io) suggests that affiliates may get compensated for driving signups, which is common in fintech but worth noting from a transparency standpoint.

- Credit-Building Products Risk

- While the credit-builder marketplace is powerful, credit-building accounts and secured credit cards are not without risk. Users must understand what fees (if any) come with those products, how they are reported, and what the real cost is.

- It’s also possible that users may take on credit products they are not fully ready for, especially if they interpret “credit building” as an easy or risk-free path.

- Marketing vs Reality

- Many of the claims are based on press releases or on-site descriptions, which have a marketing angle. As with any fintech, user experience may vary.

- There’s limited independent, third-party journalism or consumer reporting (e.g., investigative reviews, customer complaints) that validate all of CreditVana’s claims. Much of what exists is from their own PR.

- Regulatory Risk

- As a credit data platform, CreditVana must adhere to financial and data regulations (e.g., FCRA in the U.S.). If they don’t, or if their practices change, user data could be at risk, or their business model could face regulatory scrutiny.

Is CreditVana Legitimate?

Based on publicly available information:

- Yes, it appears to be a legitimate fintech company: they have a real website, a working mobile app, and documented relationships with credit bureaus.

- They have press coverage and publicly disclosed product launches (e.g., the 5.2.0 marketplace update). CreditVana

- They provide detailed information on terms of use and privacy, indicating a formal business structure. Creditvana

- Their free offering is credible and aligns with a sustainable fintech-affiliate model: give the consumer value, then generate revenue via referrals to credit products.

However, caution is warranted. Because their business model is largely based on directing users toward credit products, their recommendations may not always be purely in the consumer’s best interest. Potential users should:

- Read the privacy policy carefully.

- Understand exactly how the credit-builder accounts or cards in their marketplace work (fees, reporting, interest).

- Use their credit-monitoring alerts as a tool — but not rely 100% on their “real-time AI score” to make major financial decisions without cross-verifying.

Final Assessment

CreditVana is a very promising fintech platform for people who want to:

- Monitor their credit for free.

- Gain insight into what affects their credit (via a “report card”).

- Actively build credit by discovering appropriate credit-building products in one place.

Its strengths lie in its AI-driven insights, access to all three credit bureaus, and seamless credit-building marketplace. These features make it more than just a passive credit tracker: it’s a proactive financial wellness tool.

That said, potential users should remain vigilant about how CreditVana makes money (likely via referrals), how their data is used, and the fine print of any credit products they apply for through the app.

Conclusion:

CreditVana seems to be a legitimate, innovative, and consumer-friendly credit-monitoring platform, especially for those who are looking for a no-cost way to track their credit and improve it. If used wisely, it could be a highly valuable tool in someone’s financial toolkit.

Visit CreditVana